Government comes to bat in the middle

Government comes to bat in the middle

Telecom relief package, why Banking sector could be at a tipping point, Realty sector delivers yearly returns in a week & more...

While hitting new highs almost every other day Indian equity markets set another record of being the 6th Largest stock market in the world overtaking France for the first time. India’s market capitalization as on 14th September stood at $3.4055 Trillion ($3.4023 for France). Indian equities markets slowly but surely has become too large to be ignored by any global investor. SENSEX meanwhile scaled 60,000 mark.

Indian government took center stage this fortnight as it came out with a number of announcements impacting large sectors & businesses, some of which deserves some elaboration & explanations in this newsletter.

Telecom Relief Package: Can it stop the industry from being a duopoly ?

It needed Vodafone Idea (VIL) to head almost into a bankruptcy for the Indian government to change the definition of the contentious Adjusted Gross Revenue (AGR). Non telecom revenue will now be excluded on prospective basis from the definition. The AGR dues already pending still needs to be paid, so to ease that (somewhat) moratorium/deferment of up to 4 years in annual payments were also announced. Other major highlights from the package were 100% FDI through automatic route, spectrum sharing & single window clearance for tower installation. All telecom tycoons welcomed the relief. Media reports that Kumar Mangalam Birla (who has earlier stepped down as Chairman asking for immediate government support to prevent VIL from collapse) & Vodafone Plc. are deliberating on including fresh equity into the entity which was until few days out of the table.

We have felt that institutional investors will be wary of putting in money for equity in VIL (if it goes the QIB Fund raise route) where the money would largely be used for paying government its AGR dues, deferred spectrum license & bank debt. But the moratorium announced in relief package changes this, again somewhat. Now the equity capital raised can be directed for CapEx which VIL would need as it braces for competition with BHARTI AIRTEL & JIO both of which have already began their 5G trails. This package thus definitely breathes fire into VIL but it still needs to fix the subscriber loss that continues unabated. It clearly is not out of waters, yet.

We like to believe that these reforms doesn’t assist JIO as much as it does to BHARTI & VIL (because JIO has insignificant amount of AGR dues). And between the latter two BHARTI is better positioned with higher ARPU (Average Revenue per User) as well as sustained active subscriber growth in addition to lesser debt than VIL. No doubt markets are cognizant of these facts as BHARTI gained 30.66% YTD and trades at 52 Week high.

BANKING SECTOR: A giant getting ready to wake up

Banking sector have had a very slow run compared to major sector such as IT, METAL, REALTY, ENERGY or FMCG.

And it had it reasons. The Asset quality outlook deteriorated with COVID impacting the cash flows of customers in both the waves of COVID in India, loan growth was sluggish and spikes in slippages to name a few.

But now the things could be turning around for the better. Government announced ‘BAD BANKS’ (National Asset Reconstruction Company Limited, NARCL) where the total guarantee will be maximum of INR 30,600 Cr. This definitely improves the situation slightly for the Public Sector Banks.

Prominent names like SBI BANK looks well positioned to report strong uptick in earnings led by normalization of credit costs. Private players like HDFC BANK posted a healthy performance in Q1FY22 in spite of challenging environment, RBI also partially lifted the restriction on issuance of new credit cards just before the festive season helping it get its house in order. Others like KOTAK BANK which had poor outlook on loan book growth are actively pursuing paths to improve it like being the first in the industry to lower rates for home loans (for festive season to begin with).

And of course, the charts are at an tipping point of sorts at the current juncture and any further up move can set this giant sector rolling in the medium term.

Government gets serious about giving AIR INDIA a buyer

So it official finally! Tata Sons has submitted financial bid for AIR INDIA and so has Ajay Singh (owner SPICEJET) in his personal capacity. But government has done its bit to sweeten the deal, it is allowing suitors to decide how much of AIR INDIA’s debt they want to take from $3.3 bn. Compulsion to take on the full debt was providing significant hindrance to find a buyer for the carrier in past. The bid from group of AIR INDIA’s employees who partnered with Seychelles based fund was disqualified.

Aviation sector is seeing some rays of light with improvement in air traffic (6.7 Mn passengers in August compared to 5.01 Mn in July) as COVID cases for the timings seems to stay under control. Aviation ministry also raised the allowable flying capacity to 85%. With the sentiment around the business improving we expect the sale to be complete soon. But we like to think this would add one more competitor (and a fierce one given the backgrounds of SPICEJET & TATA) and this will have some ramification in profitability over the sector on a longer frame of time.

Festive season arrives early for REALTY Sector

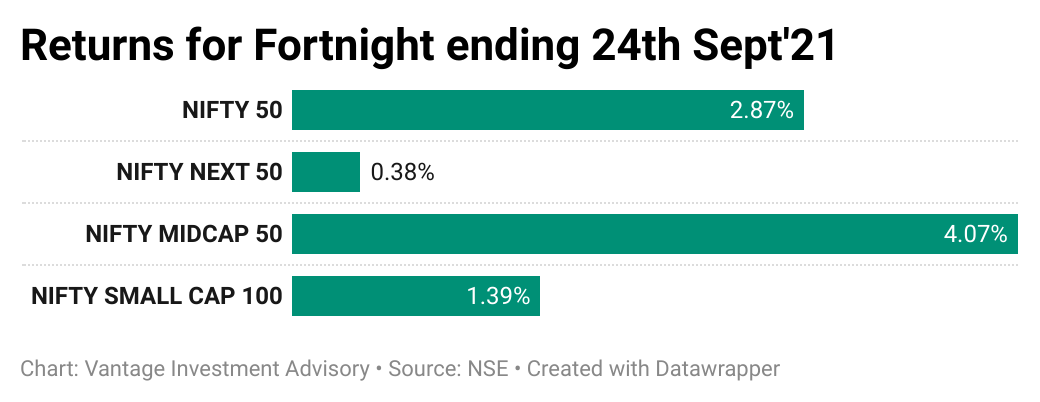

Realty index posted mammoth gain, adding 22.7% returns just in the past week. And if you are following Vantage Fortnightly you must have taken some moolah home already.

In line with our expectations many developers have preponed the launches of new projects to August-September ’21 as a response to strong buyer demand. GODREJ PROPERTIES sold INR 5.8 bn of inventory in just the very first day of the launch of its phase-2 of Woods project (in Noida). Other players are seeing similar success. We acted on this opportunity for the benefit of our members through DLF stock idea.

EVERGRANDE - after Tech its Real Estate’s turn in China

Xi Jingping is clear that relentless rise in property prices & debt must be bought to heel and wants to rein in over leveraged property companies. But he might have gone overboard with ‘common prosperity’ in the case of Evergrande. If you are unfamiliar with the much talked about Evergrande’s default situation let our tweet thread help.

China has realized that letting this property behemoth default have more ramification that they would be comfortable with. Financial regulators have issued broad set of instructions to Evergrande so that it takes all possible steps to avoid near term default on dollar bonds and focus on completing unfinished projects and repaying investors back.

Increasingly China’s financial market terrain is getting marred with more regulatory risk than the appetite of global institutional investors allows them. Outperformance of Indian market compared to its Emerging Market (EM) peers might be an leading indicator to this. But the sheer size of China’s market owing to its mammoth economy & growth prospectus might make it difficult for any other EM to move the foreign capital away China in a jiffy but a gradual move away is very much on cards.

VANTAGE LARGE CAP Model Portfolio Performance

Vantage Large Cap model portfolio was introduced into the offering for members keeping in mind the inability of most Mutual Fund’s large fund to beat index returns (read here). This also falls well in the quadrant of low volatility and high quality stocks where we focus our work & attention on. This is an ideal time to look back on the relative performance of the Model portfolio vis-à-vis benchmark since its inception (December, 2020) till date.

The stock universe is NIFTY100 (NIFTY50 & NEXT50) and model portfolio currently comprises of 16 stocks. This is low churn focused portfolio designed to help members beat markets consistently without any loading on risk.

Disclaimer: This article is for information only, and should not be considered as a recommendation to buy or sell any stocks etc. Mentioned stocks etc. maybe part Vantage Model Portfolio, Vantage Short & Medium Term investment ideas and Vantage members might have been advised on it.

Vantage Investment Advisory is a registered Investment Advisory focused around momentum & value investing in Indian Equities Markets. We are currently helping our members across 15 cities in India, US, UAE & Singapore better their investment performance with our stock picks.

If you want us to help you in your investment journey with institutional grade, crisp, clear & actionable ideas, then reply back to this email or email us on advisor@vantagewealth.in or Direct Message us on Twitter, LinkedIn or Instagram. We can also be reached on our help desk number +91 86530 15072 via Call, WhatsApp or Telegram. We will be more than happy to get in touch with you!