Market Correction elusive, Returns blatant

Market Correction elusive, Returns blatant

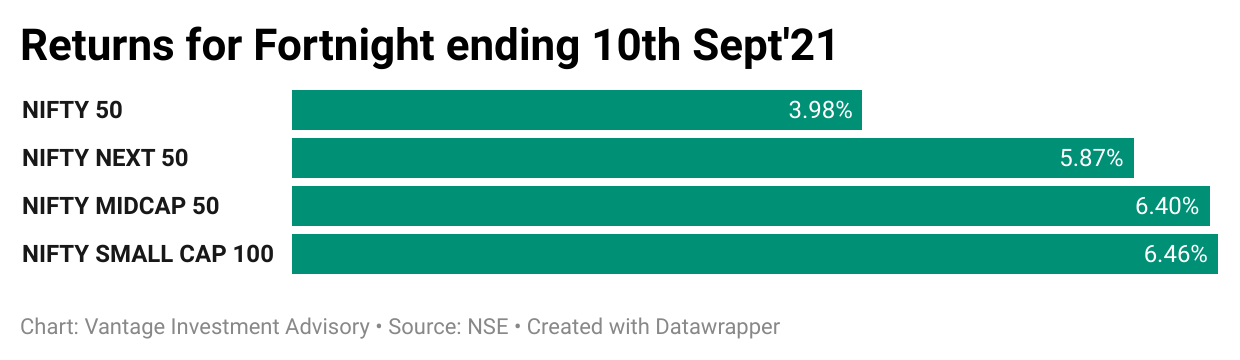

One of the most hated rally of all time in NIFTY continued unabated, adding the fastest 1,000 points in just 19 days!

We are remined of a quote by legendary fund manager Peter Lynch,

“More people have lost waiting for corrections and anticipating corrections than in the correction themselves”

As writeups, videos and interviews continued to increase on why market correction should be around the corner (corner began from NIFTY 9000 if you are wondering!) lets jump into this edition of Vantage Fortnightly and do what we do best - share high probability ideas & themes that you can use to boost your investment performance and opportunities that performed for Vantage members.

Rising Tide of Residential Real Estate

Like it or not Work From Home (WFH) is here to stay and 100% work from office is passé. Robust hiring outlook in IT/ITeS, Financial Service & Start-Ups along with spike in salary increment and wage hikes means demand pull is likely to remain strong. Add to it the fact that mortgage rates offered by most large lenders are in the range of 7-7.5% (for 20 year housing loans) which is lowest ever historically since 2005. Akin to flash sale in e-commerce, banks have started offering rock bottom rates interest rate sensing this opportunity.

For the Developers (mostly listed one’s) a plethora of factors (ranging from reduction in cost of debt, reduction in corporate overheads compared to pre-COVID, equity capital raises through QIBs etc.) helped them reduce their net debt levels. ICICI Direct pegs the reduction at 37%. These factors couple together to strengthen these developers’ balance sheet.

The aggressive project launch plans by listed (and unlisted) developers in 2nd half of FY22 gives (read about it here) us a sense that they too want to make hay while the sun shines. The consolidation in market share by larger listed players have begun and they look poised to grow in double digit (sales value).

While the narrative ‘sounds’ good, the charts ‘looks’ good. On the monthly time frame the NIFTY REALTY INDEX seems to be indicating a strong pent up momentum. This sector, to us, looks ripe with opportunities for medium term.

Insurance sector shifting gears

Total number of individual policies sold in August’21 was up by 12.3% YoY for the private sector & 26.6% YoY for the entire insurance industry. The revival in sales in June’21 post the second wave of COVID continued well into August.

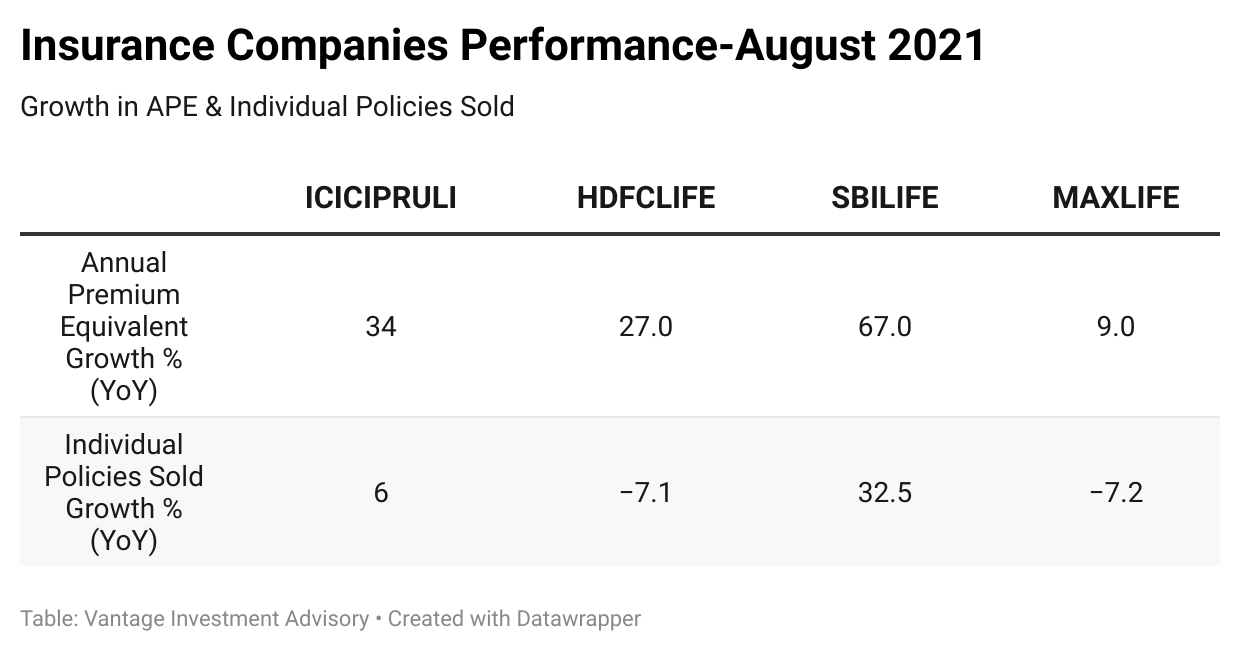

Most of the FY21 was supported by growth in traditional plans but we like to believe going forward linked products will step in to boost the revenue & margin. Below is a brief comparative snapshot of insurance companies performance in August’21.

SBILIFE is our 2nd favorite in this pack and has shown the strongest recovery (1st being ICICIPRULI where the investment idea hit its target). This recovery play was another actionable idea that we closed for our members this fortnight which delivered 15% in 1.5 month. You can read more about it here.

This space also saw the largest deal in India with EXIDE LIFE Insurance being acquired by HDFC LIFE for a total consideration of INR 6,687 Cr. Strong market presence of EXIDE LIFE in South India will provide a wider market for HDFC LIFE in addition to providing it impetus to its agency business. This development along with the fund raise plan has breathe fire into HDFC LIFE’s stock price. We are keenly tracking these development in order to leverage any opportunity that might show up.

As LIC IPO process moves into the next gear with government appointing investment bankers for the issue we are sure this sector will in the center stage for a while.

Riding on Q1FY22 Earnings momentum

We closed another short term investment idea on NAUKRI which was culmination of earning growth with price momentum (read about it here). And yes it returned 15% but in just15 days!

And finally, our medium term investment idea on ‘BRITANNIA: A Contrarian Bet’ hit its mark. You can find the investment note below.

Rapport of Rupee & (Interest) Rates!

We weren’t surprised when USD/INR tanked from 74.2 to 72.9 after Jackson Hole Symposium. You too shouldn’t have been, if you were following Vantage Fortnightly.

We believe this improves the risk-on approach of the foreign money flow and will continue to give more legs to the Indian Equities market rally.

However, US Federal Reserve has a balancing act to play now. While the clamor for reduction of monthly $120 billion bond purchase increase, change in non-farm payroll was a dismal 235,000 (vs. the forecast of 733,000) which meant US Economy added back jobs at a far slower pace than expected. All in all, US Fed would not want to rush into any change in its bond purchase program. We believe RBI would try to keep the Rupee range bound between 75-73. The next FOMC meet is scheduled on 21st September and is going to be keenly watched.

‘AIRTEL’- New kid in Vantage Model Portfolio performs

While NIFTY & Large Cap Mutual Fund beating performance of Vantage Model Portfolio continued the most recently added stock to this portfolio - BHARTI AIRTEL delivered 8.8% returns since 13th August, the inclusion of which we covered in 3rd Edition of Vantage Fortnightly (shared below). It has now announced INR 21,000 Cr Rights Issue to arm itself for launch of 5G alongside looking to retire some debt from INR 1.6 Lakh Cr.

When we say ‘This newsletter is FREE, but the ideas in it can make money’, we mean it!

T+1 Settlement Cycle is here

Since T+14 days Settlement Cycle in Harshad Mehta days (‘1992 Scam’ fame) India Equities markets have come a long way in market operation efficiency as SEBI proposed optional T+1 rolling settlement which comes into effect from 1st Jan, 2022. While you can read the complete circular here, it simply means that exchanges can decide which scrip they want to provide T+1 settlement. There is some clarity needed though on what happens if the same scrip follows 2 different settlement cycle in different exchanges. Think of it this way, you might get the stock of ICICI BANK in your demat account in 1 day if bought from NSE, but the same could take 2 days if bought on BSE.

Private Investors (Retail & HNIs) will be the biggest beneficiary. The capital utilization would be better (as the funds would be freed and stocks be available more quickly. Also the risk of inability to sell stock for 2 days is further halved which has pronounced meaning in volatile market phases.

However, we anticipate some push back from the intermediaries like custodians, brokers, banks, depositories etc. as there resources could get stretched. Also, Foreign Institutional Investors (FII) do the necessary forex transaction on T+1 day for the trade taken on T day. That in turn means the forex would need to be done before the trade is completed (given on-shore currency market sees largest liquidity in 12pm-3pm window while equity market shut only at 3:30pm).

So clearly there are issues which needs to be ironed out, but we are hopeful that this would be done sooner than later.

We hope you reached out to your favorite teachers & professors and wished them on Teachers’ day. While we did the same, we also had to thank another lifelong teacher - ‘The Markets’.

What did market teach you? We would love to hear that from you. Feel free to leave a reply or comment on what you would want us to write on next.

Disclaimer: This article is for information only, and should not be considered as a recommendation to buy or sell any stocks etc. Stocks etc. mentioned maybe part Vantage Model Portfolio, Vantage Short & Medium Term investment ideas and Vantage members might have been advised on it.

Vantage Investment Advisory is a registered Investment Advisory focused around momentum & value investing in Indian Equities Markets. We are currently helping our members across 15 cities in India, US, UAE & Singapore better their investment performance with our stock picks.

If you want us to help you in your investment journey with institutional grade, crisp, clear & actionable ideas, then do email us on advisor@vantagewealth.in or DM us on Twitter, LinkedIn or Instagram. We can also be reached on our help desk number +91 86530 15072 via Call, WhatsApp or Telegram. We will be more than happy to get in touch with you!