Markets 'powers' ahead, but power runs short elsewhere

Markets 'powers' ahead, but power runs short elsewhere

Glittering TITAN, if you should subscribe to AIRTEL Rights, market makes peace with SEBI Margin regulation & TATA buys Air India. BONUS: A stock idea for you!

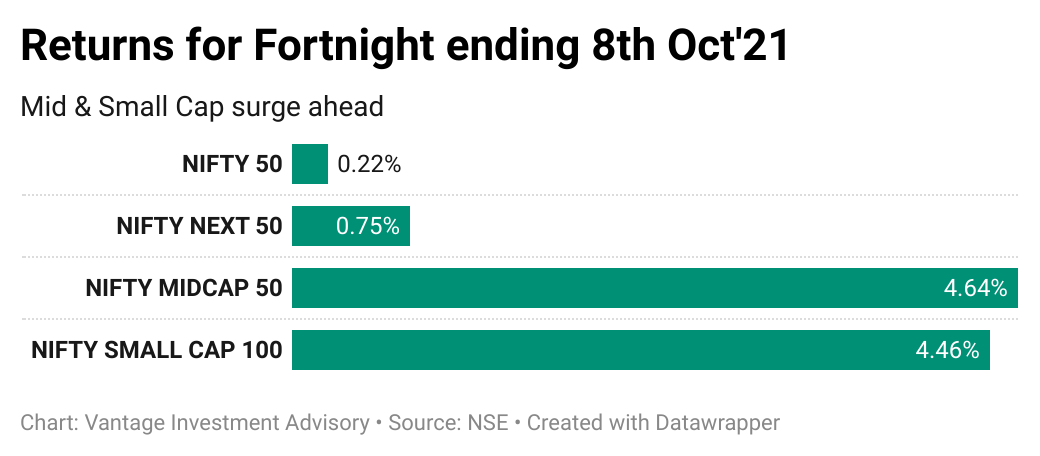

Last fortnight has been all about the imminent power shortages. Lack of coal & natural gas threatens to derail economic recovery of China as it stares into power crunch. In USA, Natural Gas jumped to the highest price in 12 years. Back home media articles reports power plants having coal supply of just a handful days left with some State(s) sending SoS to Central government.

Markets however saw no dearth of power (or gas!) as it closed at new high.

All that glitter is TITAN : beats street estimate significantly

Q2FY22 was off to a strong start with TITAN (Vantage Large Cap Model Portfolio stock) delivered a stupendous quarter. Standalone revenue (excluding gold bullion sale) grew 78% YoY beating analyst estimate of 40%. It continued its march to gain market share with an impressive 2 year CAGR of 32% surpassing pre-COVID levels in H1FY22 with growth of 16%. Watches reported 73% YoY growth with healthy momentum while walk-ins gradually gathering pace. These growth jumps were definitely assisted by demand revival but TITAN’s strategy of robust balance sheet & asset light distribution provided the base. Staying asset light means it can continue to outpace peers in terms of store addition. Mandatory gold hallmarking is expected to further enhance market share which has immense opportunity to grow given the nascent stage Tanishq is still in. Softening of gold prices with a strong pent up demand for the upcoming wedding & festive season is only going to boost the topline for Co. The bull case for stock only grows stronger from here.

We in our Large Cap Model portfolio (targeted to beat NIFTY50 & Large Cap Mutual Fund) introduced TITAN on 5th May and since then it has delivered 66.78% for our members.

If you aren’t a member yet and want to jump on to such ‘multi-baggers’ in plain sight at favorable entry points consider reaching out to us (by simply replying back to this email).

Market swallows SEBI margin regulation with ease

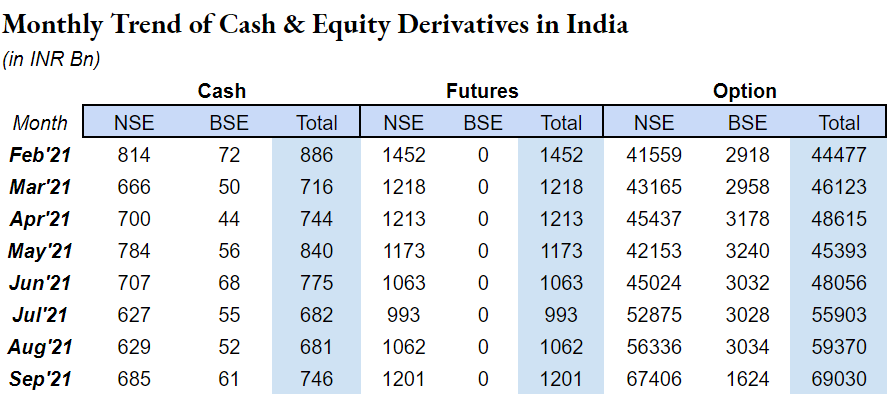

To the uninitiated, under the SEBI’s new peak margin rule traders would require 100% margin upfront for any trades. This was implemented in a phased manner with the requirement of 25% peak margin till February’21, 50% till May’21, 75% till August’21 and fill stage of 100% from September onwards. This meant if you wanted to even do any intraday trading you would need to bring to the table entire margin money since start of September. A lot of market participants (including us) expected that the new margin regime bought into force from September would hamper the volume and in turn the liquidity in Indian Equities & Derivatives market.

The volume data however indicates that market was more than prepared to handle this regulation.

While volume (data in table is in value terms) has more or remained around the same range, the growth in options market has been pronounced. Either ways the fear of market liquidity being impacted massively has been largely allayed. We are of the view that whatever impact has come will more than be offset by T+1 settlement cycle that has being seeing increased clamor of implementation from various intermediaries after the proposal from SEBI.

Curious case of BHARTIARTL Rights Entitlement - Should you subscribe?

BHARTIARTL which has recently announced its rights issue of INR 21,000 Crores. If you are a shareholder of the stock you should find the Rights Entitlement (RE) in your trading account (1 RE for every 14 stocks held before the record date).

But what should you do with this RE: Sell it off while its trading (till 14th Oct’21), buy more of it or just hold and pay the first call (INR 133.75) and the own partly paid shares of BHARTIARTL?

Lets look at few small calculations:

BHARTIARTL Rights Issue Price = INR 535

CMP RE = INR 208.75

Effective Price for Buying BHARTIARTL = INR 535+208.75 = INR 743.75

CMP BHARTIARTL = INR 695.5

Current discount = 743.75-695.5 = 48.25INR

Clearly the stock is trading in market at a discount to the effective price that the Rights issue is factoring in.

We do concur that only 133.75 is called for right now and the remaining 2 calls will be made anytime in next 36 months. So the balance INR 401.25 will sit in a liquid instrument/savings bank account. Assuming a 3% interest rate at the end of 3 years (translating into 9.27% over 3 years) translates in INR 438.45 or an interest income of INR 37.2 which is still clearly less than the current discount.

Additionally, given the CapEx plan that the Co. has for itself for 5G trails & network expansion along with the debt schedule, its very likely that these next 2 call will be much before the end of 36 months. Making subscribing to these REs even more unattractive.

Vantage Fortnightly Stock Idea - INDIAMART INTERMESH

Current Market Price: 8805

Time Frame: Medium Term (4-5 Months)

Expected Upside: 20-25%

Why we like INDIAMART?

1. The management had said in Q1FY22 earnings call that it aims to grow from the current level to 5x-10x in the next 5-10 years. It has also made it clear that it will not shy away from inorganic growth if the the business align and help them consolidate their position in the platform business along with organic approach. It has invested very recently in 3 companies - 11% in Legistify.com (SaS tool to help enterprise to manage legal work flows), 25% in TruckHall (SaS based tool to help large companies manage supply chain & real time based freight sourcing and collaboration platform) & 26% in Shipway.in (SaS based solution for business to automate their shipping operations).

2. Seeing the trend that apart from its traditional one-on-one meeting people have started using telephone & online more, the company has now channel partner to acquire customer. 25% of customers acquired are through this channel already. This can give big boost to top line as it expands its influence over time.

3. Various cost optimization measures that has been implemented is already showing positive effect (like EBITDA margin of 48.8% in Q1FY22) and is likely to show a much more pronounced impact in coming quarters.

4. Its ARPU (Average Revenue per User) has been consistently increasing from INR 44,600 in Sep’19 to INR 49,700 in Jun’21. Throughout this phase it hardly have any meaningful down-move in its ARPU.

5. The stock has gone into a sideways correction followed by a very narrow band of consolidation for about 6-7 months and out in-house proprietary analysis indicate early signs of momentum returning back in the stock.

Investment Risks

1. Reliance has freshly infused capital in it and this can shift Just Dial’s focus from monetization to disrupt the industry on pricing and try to catch up B2B aspect of the business.

2. At a PE of 91.81 the valuation comfort is significantly low.

AIR INDIA flies home to TATA

In line with our expectation (you can read more about it in our previous edition of Vantage Fortnightly below) government was indeed successful in finding a buyer and it was TATA Group, the group which originally owned the airlines.

The deal sweetener worked wonderfully well. TATA group which bid INR 180 bn as Enterprise Value will retain INR 153 bn of AIR INDIA’s debt & pay INR 27 bn cash to government. The balance debt of INR 462.6 bn will be retained by Indian government in a Special Purpose Vehicle (SPV).

All’s well that ends well.

And finally we wanted to share with all our readers a small milestone that we reached. It would not be possible without the support, encouragement, motivation and feedback from each one of you which enabled us to travel this far in just 10 short months.

Thank you!

PS: If you believe we could help you with your investments feel free to reply back to this email. We would love to hear from you.

Disclaimer: This article is for information only, and should not be considered as a recommendation to buy or sell any stocks etc. Mentioned stocks etc. maybe part Vantage Model Portfolio, Vantage Short & Medium Term investment ideas and Vantage members might have been advised on it.

Vantage Investment Advisory is a registered Investment Advisory focused around momentum & value investing in Indian Equities Markets. We are currently helping our members across 15 cities in India, US, UAE & Singapore better their investment performance with our stock picks.

If you want us to help you in your investment journey with institutional grade, crisp, clear & actionable ideas, then reply back to this email or email us on advisor@vantagewealth.in or Direct Message us on Twitter, LinkedIn or Instagram. We can also be reached on our help desk number +91 86530 15072 via Call, WhatsApp or Telegram. We will be more than happy to get in touch with you!